2019 State of Logistics: Third-party logistics (3PL) providers

State of 3PL: More mergers and aquisitions on the horizon

The global third-party logistics (3PL) market is estimated to reach $1.3 trillion by 2024, registering a strong compound annual growth rage over the forecast period, say industry analysts. A steady increase in the need to meet growing e-commerce penetration continues to act as one of the key drivers.

However, this bullish forecast by Research and Markets, a Dublin, Ireland-based consultancy, is tempered somewhat, with the acknowledgement that some 3PLs have experienced “loss of control over the shipping functions,” which could be a major restraint to the market.

According to Catriona Rigley, research manager at Research and Markets, Asia was the top contributor to trade growth in terms of volume so far this year, growing by 8%. Furthermore, Asia saw steady year-on-year growth in imports throughout 2018.

According to Catriona Rigley, research manager at Research and Markets, Asia was the top contributor to trade growth in terms of volume so far this year, growing by 8%. Furthermore, Asia saw steady year-on-year growth in imports throughout 2018.

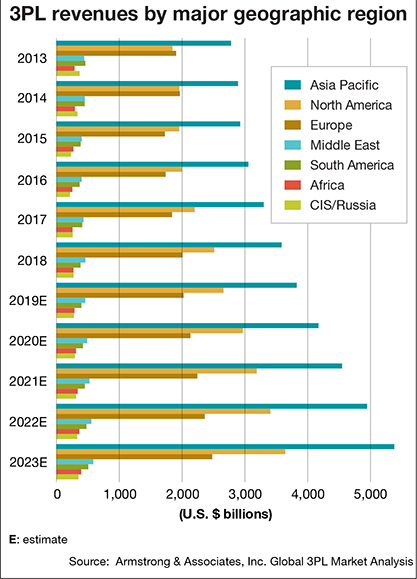

Asia also recorded the highest growth in merchandise trade volume in 2018 for exports (6.7%) and imports (9.6%), following two years of modest expansion. The region contributed 2.3% to the global growth of 4.5% in 2018, or 51% of the total increase. Asia also contributed 2.9% to the world import growth of 4.8%, or 60% of the overall increase. Last year, Asia-Pacific’s third-party logistics market was estimated to be $329.3 billion.

“The global 3PL market is highly competitive with the presence of major international players, like Agility, CEVA, DB Schenker, and DHL, among others, trying to capture significant market shares,” observes Rigley. “The industry exhibits shifting patterns and this has allowed new competitors to enter the market and challenge the existing players.”

According to Rigley, 3PLs have shown the willingness to partner with other players to reduce cost and leverage on mutual competitive advantage. Hence, the market observes a high volume of ongoing mergers, and acquisitions.

“The global 3PL market players are also observing a shift in technology with the development of artificial intelligence, Internet of Things (IoT), and Blockchain, among others,” says Rigley. “The introduction and implementation of these new technologies have further intensified the market competition. Additionally, the technology adoption also helped reduce operational costs and improved efficiency.”

Greg Aimi, vice president and team manager at Gartner, agrees that the 3PL industry is progressing along “a maturity spectrum,” and is trying hard to accommodate increasing shipper requirements through a combination of acquisitions, organic growth strategies and investments in innovation—such as digital technologies and processes.

“However, our research shows that not all 3PLs are at the same place in their journey,” he says. “Many companies view logistics outsourcing as an effective strategy primarily to reduce costs, but more and more shippers are seeking innovative solutions that can improve process and service as well.”

Courtney Rogerson, senior principal analyst with Gartner, and co-author of this year’s “Magic Quadrant for Third Party Logistics, North America,” adds that mergers and acquisitions are a very common growth strategy, and consolidation is likely to continue as it presents a faster way to obtain more services and provide coverage in additional geographies than organic growth.

“In that regard, as evidenced by recent events, shippers should be aware that a 3PL provider of almost any size could be involved in a change of ownership,” Rogerson concludes.

Read the feature article on the 2019 State of Logistics here.

Article Topics

3PL News & Resources

Port of Los Angeles and Port of Long Beach monthly volumes head up again BlueGrace Logistics Confidence Index sees signs of stabilization for the third quarter Assessing the freight recession and truckload market with Mike Regan, TranzAct Technologies FTR’s Trucking Conditions Index falls to lowest level since last September Cass Freight Index points to annual shipments and expenditures declines U.S.-bound import growth remains intact in April, reports Descartes Looking at a reshoring history lesson More 3PLLatest in Logistics

Packaging Efficiency: The modern way to reduced freight costs Port of Los Angeles and Port of Long Beach monthly volumes head up again National diesel average drops nearly 6 cents, for lowest reading since July, reports EIA Baltimore Bridge Collapse: Dali cargo ship is finally on the move Bloomberg/Truckstop 1Q24 Truckload Survey points to improving spot market sentiment BlueGrace Logistics Confidence Index sees signs of stabilization for the third quarter Assessing the freight recession and truckload market with Mike Regan, TranzAct Technologies More LogisticsAbout the Author

Subscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

May 2024 Logistics Management

Latest Resources